Marguerite Morrin* outlines how new energy sectors are supporting a strong growth in soda ash demand.

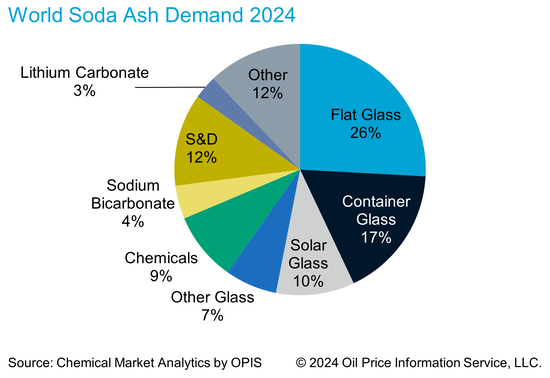

Soda ash plays a key role in numerous industrial sectors with glass accounting for approximately 60% of world consumption.

Flat glass is the largest glass segment and container glass, the second largest (Fig 1). Solar glass, used in solar panels, is the single fastest growing demand sector.

In 2023, world soda ash demand grew by 2.7%, 1.8 million mt, this increase was driven by China.

In 2023, growth in China was the highest on record, 10%, or a net increase of 2.9 million mt. World demand, excluding China fell by 3.2%.

Fig 1. Global soda ash demand in 2024.

Soda ash supply

Soda ash capacity was fairly static between 2018 and 2022, as many expansions that had been planned were delayed due to Covid-19. In fact, during this time period, there was a net loss in capacity in China.

However, the most significant expansions in the near term have been in China, including 5.0 million mt of new low cost (natural) production which started ramping up in mid-2023.

The biggest recent expansions in the US were both by Genesis, where a total of approximately 1.2 million mt of capacity was operational at the end of 2023.

By 2028, 18.0 million mt of new capacity is scheduled to be added globally, 61% of the additions are in China and 34% in the US.

As capacity is added the technology base is also changing. Natural soda ash is accounting for a growing share of the new capacity. Its share of the world total is forecast to reach 22% by 2028.

Natural soda ash production is typically much lower cost than synthetic. As such, the changing technology profile is also changing the global cost curve. Competition is on a delivered basis and the geographical location of where capacity is being added will also impact on competitiveness.

Fig 2. Soda ash import trends in Asia.

Demand growth

Soda ash is a basic chemical that serves end use sectors which are important in our everyday lives. As a consequence, demand growth has traditionally been driven by developing economies. But demand is no longer just being driven by economic growth, it’s also getting a huge boost from environmental sectors.

However, the absolute potential for soda ash into these end use applications can be difficult to forecast. The outlook for soda ash consumption for batteries, including lithium-ion batteries, is complex.

The same is true for solar glass as various international energy bodies are continually revising up their projections for solar power.

Trade

In the soda ash industry trade plays a pivotal role, as centres of production are not always located in close proximity to regions of high demand, and approximately a quarter of soda ash is shipped between key regions.

The US, Türkiye and China are important countries in the sector due to their influence on the seaborne market. For US producers, demand in the export market drives more growth than the domestic market, which is mature.

Historically, US producers have raised production through an increase in exports, aided by a competitive cost structure. Key seaborne markets include Other Asia (excludes China and India Subcontinent) and South America.

The US is the biggest soda ash exporter in the world. Türkiye is in second place.

Although China’s share of global trade is relatively low, it has a big impact on the health of the global soda ash market because of its volatile exports, an example of which we’re seeing to date this year.

As mentioned, China added considerable capacity in 2023 and into 2024 – this created expectations of surplus availability, yet imports to China in H1 2024 were the highest on record.

Meanwhile, in January-May this year US exports were up by 13%, year-on-year; the biggest volume increase was to China.

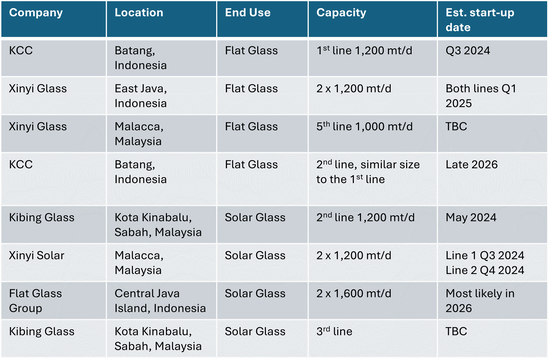

Fig 3. Solar and flat glass projects scheduled for Indonesia and Malaysia.

Role of China

The extremely strong demand growth in China in 2023 took demand to around 31.4 million mt – it was driven primarily by solar glass.

There is to be a net increase in soda ash capacity in China of 5.5 million mt in 2024, which is in excess of short-term expectations for new demand.

However, demand growth to date this year is once again exceeding expectations with demand in the first six months of 2023 up by 27%, year-on-year. If the current level of growth is maintained, the gap between supply and demand in China will no longer be excessive.

Solar glass production in China grew from 16 million mt in 2022 to 25 million mt in 2023.

The country has continued to expand its solar glass and by July 2024, the total capacity was about 46 million mt.

However, the Chinese authorities are concerned about over-capacity in solar glass and are in talks about introducing restrictive policies. Meanwhile, according to the National Energy Administration (NEA), photovoltaic (PV) installations in China in January-May 2024 grew by 29%, year-on-year.

However, the PV module sector in China is reported to be operating at a loss, causing some small-scale assemblers to idle or even terminate production.

Meanwhile, a large number of PV module assemblers in Southeast Asia, mainly owned by Chinese investors, are important suppliers to the US PV market.

A number of these assemblers are reported to have stopped production recently due to the lifting of an import tax holiday by the US government. Southeast Asian countries are in turn a major export destinations for China solar glass.

Rest of world

While soda ash demand growth in China is at record high levels, soda ash demand developments outside China are more varied. The summaries below of demand in Other Asia and the Americas describe some of these trends.

Fig 4. Soda ash import trends in the Americas.

Other Asia

With little local capacity, import statistics provide a useful indicator for soda ash demand trends in Other Asia (excludes China and India Subcontinent).

Imports to this region in the first 5-6 months of 2024 reached 2.0 million mt, up by 4.7%, year-on-year (Fig 2).

Solar glass is a key driver for soda ash demand in Other Asia, with flat glass also having the potential to contribute positively.

A number of solar and flat glass projects are scheduled for this region, as described in Fig 3, which have the potential to add about 1.0 million mt of new soda ash demand.

However, there are some challenges in the solar glass industry. Recent US tariffs, including anti-dumping and anti-subsidy duties, may impact PV module production in countries such as Vietnam and Malaysia.

The tariffs, which target Chinese-made components, require manufacturers in these countries to source key sub-components from non-China suppliers to avoid hefty duties. This increases production costs and complicates supply chains which will reduce the competitiveness of Southeast Asian PV modules in the US market.

As a result of these tariffs, several Chinese-owned PV module assemblers in Southeast Asia are said to have stopped production in June with further production likely to be suspended in the coming months.

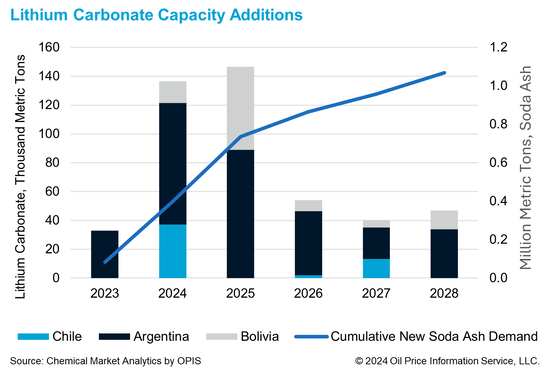

Fig 5. Lithium carbonate capacity additions from 2023 to 2028.

The Americas

The Americas region (excluding the US) has a huge reliance on imports. As such, the overall change in imports provides a good indicator of underlying demand.

The latest available trade data reflects a negative trend with imports for the first 5-7 months of the year, down by 12%, or 285,000 mt (Fig 4).

The biggest decline to date was in North America, down 23%, or 148,000 mt, led by Mexico. Container glass, the single biggest soda ash demand sector in Mexico, is weak, on the back of muted demand for alcoholic beverages. Overall soda ash demand in Mexico is not expected to improve until 2025.

The decline in South America has also been steep; down by 10%, year-on-year. The main weakness has been in Argentina where imports were down by 63%, year-on-year.

Imports to Argentina should though improve as the year progresses as there are a number of new lithium projects scheduled to come on stream (Fig 5).

In fact, lithium carbonate is by far the biggest demand driver for soda ash in South America. And while there is some negative sentiment around the lithium sector of late, the medium/long-term prospects seem positive as a low-cost producing region.

Fig 6. Soda ash export price comparison from 2010 to 2024.

Prices

Export prices from the key suppliers reflect the changed global market dynamics (Fig 6). Prices from China are typically the most volatile.

In 2023, export prices from China averaged $360 per mt FOB, prices started 2024 at $301 per mt FOB, falling to $264 per mt FOB by June.

Meanwhile, export prices from Türkiye started 2023 at $386 per mt FOB, reaching just $211 per mt FOB in December 2023 and $193 per mt FOB in May 2024.

In January-May 2024, the US export price averaged $230 per mt FAS down from an annual average of $298 per mt FAS in 2023.

Conclusion

In conclusion, only a short time ago there was seen to be looming over-capacity in the soda ash industry. However, the potential surplus may not be as extreme as feared if the demand growth which is being observed in China is maintained.

However, this growth is coming from the clean energy sectors and the absolute demand potential in this category is difficult to accurately predict.

World Soda Ash Conference

Chemical Market Analytics by OPIS, a Dow Jones company, will host the 17th annual World Soda Ash Conference, this October (9-11th) in Malta. The conference theme is: The Soda Ash Market Paradox.

At World Soda Ash (see left), global experts and industry executives from all market sectors will convene to hear expert forecasts for the soda ash industry and allied industries, discuss market dynamic challenges and opportunities, and explore the influence of evolving global market trends, including how Chinese markets will impact the world.

Glass International readers can use the code GLASS10 for a 10% discount off the conference pass rate.

For more information on the conference, please scan the QR code below:

*Executive Director, Chemical Market Analytics by OPIS, Maryland, USA